ESG

Sustainable Investing Newsletter published on April 1, 2022

Sustainable Bond Issuance Is Growing Across Bond Market Segments

Summary

- Sustainability bond issuance totaled $10.6 billion in February, 2022, 60 percent higher year-over-year.

- Increasing issuance illustrates the market’s favorable view of sustainable bonds.

- Broadening use of green, social, sustainable, and sustainability-linked bonds across bond market segments suggests continued growth in the years ahead.

A consistent increase in issuance during early 2022 demonstrates the market’s continued favorable view of sustainable bonds. In this article, we provide an update to our April 2021 assessment of the sustainable bond market.

Sustainability bond issuance totaled $10.6 billion in February, 60 percent higher year-over-year.1 So far this year, according to data compiled by Bloomberg,2 companies and governments globally have raised about $94 billion in green bonds, the environmental bonds that comprise one component of the sustainable bond market. That record pace surpasses the more than $86 billion borrowed in the same period last year.

“It’s a pretty amazing thing to see how much capital is coming in, and yet we’re just getting started. You’re going to see a lot of action,” said Brian Moynihan, chief executive officer of Bank of America Corp., the second-largest underwriter of green bonds, according to Bloomberg

Issuers of sustainable bonds—including green, social, sustainable, or sustainability-linked bonds—commonly use proceeds for eligible projects or to improve environmental, social, and governance (ESG) metrics or performance.

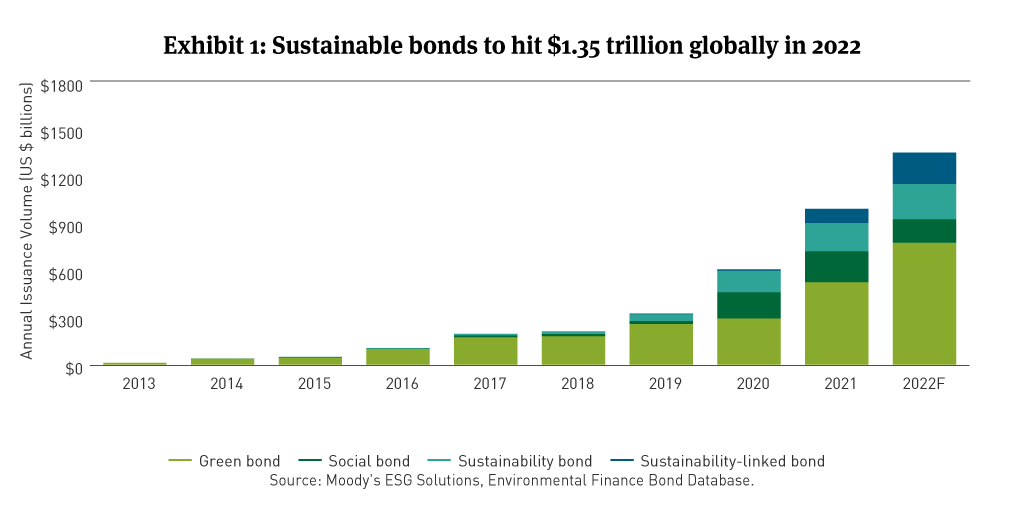

Moody’s estimates that sustainable bonds sales will hit $1.35 trillion in 2022 (See Exhibit 1). U.S. dollar denominated bonds comprise more than a third of the global sustainable bond market (See Exhibit 2).

Sustainable bonds on the rise in municipal markets

While historically corporate sustainable bond issuance leads the pack, Standard & Poor’s sees municipal green, social, and sustainable bond issuance surpassing $60 billion in 2022.3 A municipal market segment that has seen solid growth in social and sustainability bonds issuance is affordable housing projects, for example. One entity issued $4.2 billion in 54 social-labeled bonds in 2021.

Generally, investors look at the use-of-proceeds for essential service municipal debt as being aligned, at least philosophically, with many sustainable goals. Bonds can be viewed as having objectives aligned with sustainability themes if they are issued to fund environmental projects, such as coastal erosion protections or inner-city heat islands, or social programs, including education or water and sewer services, for example. For this reason, the essentiality of municipal projects generally align well with green, social and sustainable-labeled debt.

An important step in broadening interest in sustainable bonds among investors across retail and institutional segments is providing adequate disclosures in offering documents, thereby addressing the needs of both ESG impact investors and those focused on ESG research as a risk mitigation tool. Investors seek clear insight into the use-of-proceeds for sustainable issues, to avoid greenwashing, and to monitor performance of the bonds and the projects they seek to support.

Efforts to consider improvements to disclosures about green, social, and sustainable bonds in the municipal market are underway. While the Securities and Exchange Commission promotes full public disclosure and protects investors against fraudulent and manipulative practices in the market, at the end of 2021, the Municipal Securities Rulemaking Board distributed a request for information to solicit public input on ESG practices in the municipal securities market. In response, Breckinridge submitted a comment letter in support of standardized, sector-based disclosure of material ESG information in municipal primary offerings and continuing disclosure materials. The National Federation of Municipal Analysts also formed working groups on green bond disclosures, development of a Green Bond Survey, and for recommended best practices for public power and state revolving loan funds. Breckinridge has been actively involved in the green bond disclosure working group. Finally, to support the continued development of the sustainable bond market, Breckinridge joined the Advisory Council for the International Capital Market Association’s Green and Social Bond Principles.

Securitized and sovereign bond issuers view sustainable bond opportunities

Issuers in the securitized and sovereign segments of the bond market also are poised could increase offerings designated or labelled as sustainable bonds, depending on the underlying securities.

The Federal National Mortgage Association (Fannie Mae), an MBS issuer, developed a Sustainable Bond Framework for offerings, with proceeds financing projects benefiting environmental (green debt) or societal (social debt)) goals or a combination of those two benefits (sustainable debt). These characteristics are features on the loans that underly Fannie Mae’s MBS offerings.

In ABS to date, labelled ESG issuance is limited. The approximately $9 billion of issuance in 2021 is small when compared with the $270 billion in total ABS issuance.4 The Structured Finance Association ESG task force is developing market consensus disclosures for securitization with a goal of delivering a framework in 18 to 24 months. The effort could encourage additional sustainable bond issuance in ABS sectors.

Sovereign bond issuers also are expanding their involvement in sustainable bonds. Furthermore, since Poland issued the first sovereign green bond in December 2016, more countries have been entering the market. Sovereign GSS issuance grew from $10.7 billion in 2017, to $17.5 billion in 2018 and $21.8 billion in 2019, and reached $40.5 billion in 2020, according to data compiled by Moody’s Investors Service and Environmental Finance.5

Even in a year of subdued bond issuance, managers are finding opportunities in the sustainable bond markets, thanks to investor appetite for bonds with sustainable labels as well as efforts to strengthen disclosures across sustainable bond market sectors. Sustainable bonds offer managers a broader opportunity set of green, social, sustainable, and sustainability-linked bonds for strategies that follow or align with ESG risk mitigation and impact approaches.

[1] “Sustainability Issuance Jumps as Social Bonds, ESG Loans Flop,” Bloomberg, March 4, 2022.

[2] “Bank of America’s Moynihan Sees Strong Demand for Green Debt,” Bloomberg, March 10, 2022.

[3] “U.S. Municipal Sustainable Debt Issuance Could Surpass $60 Billion In 2022,” S&P Global Ratings, February 10. 2022.

[4] Bank of America Securities, December 2021.

[5] “Sustainable Bond Insights 2021,” Environmental Finance, 2021.

DISCLAIMER

This material provides general and/or educational information and should not be construed as a solicitation or offer of Breckinridge services or products or as legal, tax or investment advice. The content is current as of the time of writing or as designated within the material. All information, including the opinions and views of Breckinridge, is subject to change without notice.

Any estimates, targets, and projections are based on Breckinridge research, analysis, and assumptions. No assurances can be made that any such estimate, target or projection will be accurate; actual results may differ substantially.

Past performance is not a guarantee of future results. Breckinridge makes no assurances, warranties or representations that any strategies described herein will meet their investment objectives or incur any profits. Any index results shown are for illustrative purposes and do not represent the performance of any specific investment. Indices are unmanaged and investors cannot directly invest in them. They do not reflect any management, custody, transaction or other expenses, and generally assume reinvestment of dividends, income and capital gains. Performance of indices may be more or less volatile than any investment strategy.

Performance results for Breckinridge’s investment strategies include the reinvestment of interest and any other earnings, but do not reflect any brokerage or trading costs a client would have paid. Results may not reflect the impact that any material market or economic factors would have had on the accounts during the time period. Due to differences in client restrictions, objectives, cash flows, and other such factors, individual client account performance may differ substantially from the performance presented.

All investments involve risk, including loss of principal. Diversification cannot assure a profit or protect against loss. Fixed income investments have varying degrees of credit risk, interest rate risk, default risk, and prepayment and extension risk. In general, bond prices rise when interest rates fall and vice versa. This effect is usually more pronounced for longer-term securities. Income from municipal bonds can be declared taxable because of unfavorable changes in tax laws, adverse interpretations by the IRS or state tax authorities, or noncompliant conduct of a bond issuer.

Breckinridge believes that the assessment of ESG risks, including those associated with climate change, can improve overall risk analysis. When integrating ESG analysis with traditional financial analysis, Breckinridge’s investment team will consider ESG factors but may conclude that other attributes outweigh the ESG considerations when making investment decisions.

There is no guarantee that integrating ESG analysis will improve risk-adjusted returns, lower portfolio volatility over any specific time period, or outperform the broader market or other strategies that do not utilize ESG analysis when selecting investments. The consideration of ESG factors may limit investment opportunities available to a portfolio. In addition, ESG data often lacks standardization, consistency and transparency and for certain companies such data may not be available, complete or accurate.

Breckinridge’s ESG analysis is based on third party data and Breckinridge analysts’ internal analysis. Analysts will review a variety of sources such as corporate sustainability reports, data subscriptions, and research reports to obtain available metrics for internally developed ESG frameworks. Qualitative ESG information is obtained from corporate sustainability reports, engagement discussion with corporate management teams, among others. A high sustainability rating does not mean it will be included in a portfolio, nor does it mean that a bond will provide profits or avoid losses.

Net Zero alignment and classifications are defined by Breckinridge and are subjective in nature. Although our classification methodology is informed by the Net Zero Investment Framework Implementation Guide as outlined by the Institutional Investors Group on Climate Change, it may not align with the methodology or definition used by other companies or advisors. Breckinridge is a member of the Partnership for Carbon Accounting Financials and uses the financed emissions methodology to track, monitor and allocate emissions. These differences should be considered when comparing Net Zero application and strategies.

Targets and goals for Net Zero can change over time and could differ from individual client portfolios. Breckinridge will continue to invest in companies with exposure to fossil fuels; however, we may adjust our exposure to these types of investments based on net zero alignment and classifications over time.

Any specific securities mentioned are for illustrative and example only. They do not necessarily represent actual investments in any client portfolio.

The effectiveness of any tax management strategy is largely dependent on each client’s entire tax and investment profile, including investments made outside of Breckinridge’s advisory services. As such, there is a risk that the strategy used to reduce the tax liability of the client is not the most effective for every client. Breckinridge is not a tax advisor and does not provide personal tax advice. Investors should consult with their tax professionals regarding tax strategies and associated consequences.

Federal and local tax laws can change at any time. These changes can impact tax consequences for investors, who should consult with a tax professional before making any decisions.

The content may contain information taken from unaffiliated third-party sources. Breckinridge believes such information is reliable but does not guarantee its accuracy or completeness. Any third-party websites included in the content has been provided for reference only. Please see the Terms & Conditions page for third party licensing disclaimers.